admin

This user hasn't shared any biographical information

“Do not lie down but stand up and fight them!"

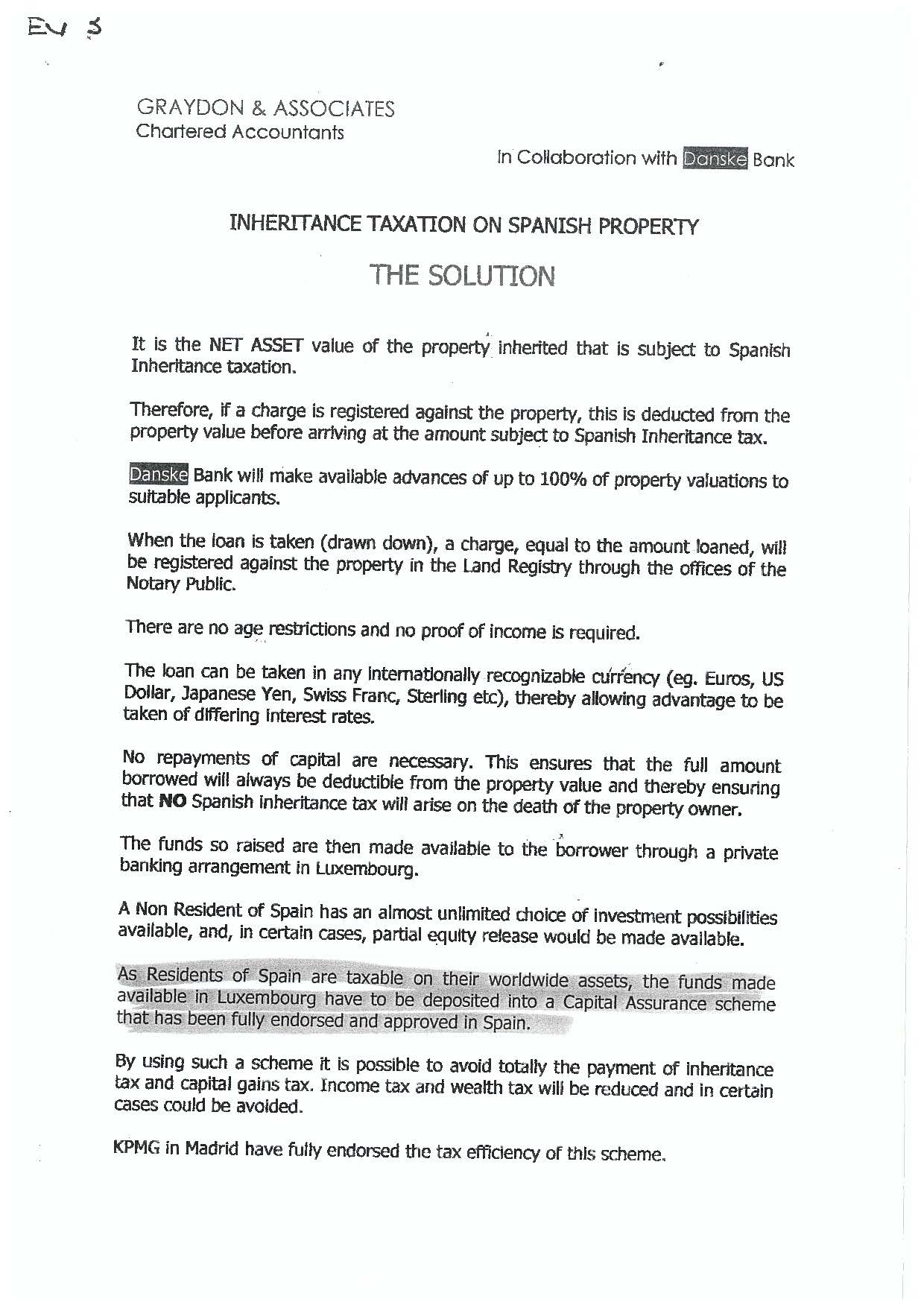

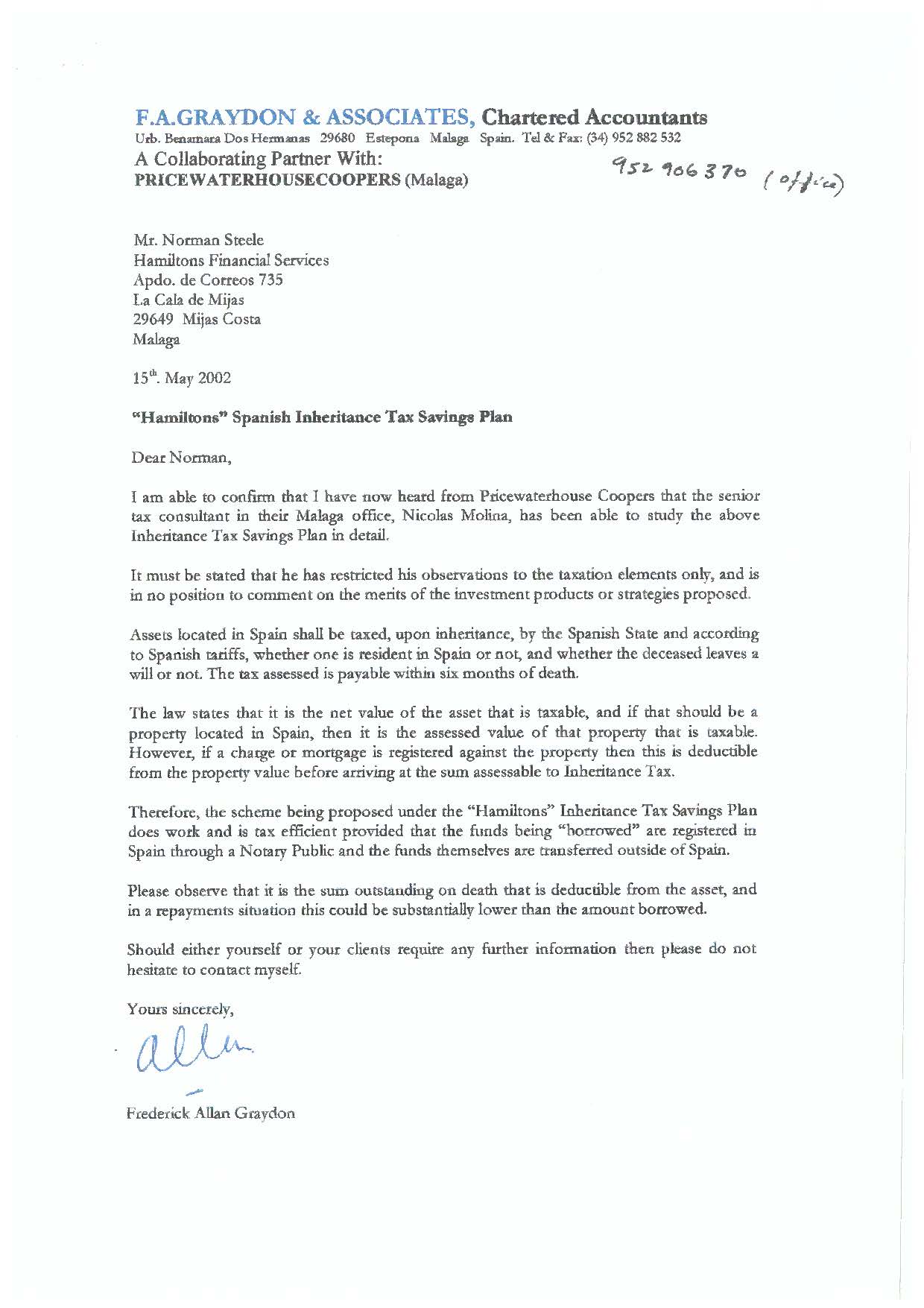

Allan Graydon, the Chartered Accountant that was not, established fruitful relationships with reputable entitiesto sell Equity Release schemes.

Jyske Bank Gibraltar is one of those financial entities that we can say has been, for some time now, sailing a little too close to the wind.

The latest scandal in the making is the proposed eviction of a Spanish resident lady, called Anne (pictured), who somehow managed to become eligible for a loan of €550,000 after presenting her credentials to the bank: survivor of several cancer operations (the last one 2 months prior), jobless, resident of Spain, never registered with the Social Security and with a meager €150/week pension from Belgium.

This form of predatory lending is certainly unknown in Spain where mortgage scandals generally relate to 120% loan-to-value mortgages, abnormal assessment of debt-to-income ratios of borrowers and other similar excesses.

Jyske has done that and more: they have lent where there was absolutely no physical possibility to repay (so much so that the Anne could not even cover the first repayment), have used an illegal company in Spain to assess its value (i.e. not registered with the bank of Spain) and moreover, have been happy with a valuation on the property next door because they could not find keys to the one transacted! Such a display of Nordic efficiency so that they could give out €550,000, seemingly in desperation to lend, to a convalescing jobless 62-year old lady (66 now) who already owned her little apartment outright -mortgage free-, and who thanks to Jyske would enjoy the benefits of a 35 year repayment plan (last repayment when she reached 97).

When Anne’s ex-husband found out what Jyske, and his ex too (!), were up to, he tried to prevent the mortgage loan from being signed by addressing a letter to Mr. Christian Bjorlow, Jyske’s Managing Director at the time of the infamous event, who rhetorically (or rather sarcastically we would add) responded by manifesting, in obvious incoherence with the financial status of the borrower, that:

“No responsible lender should grant a loan unless it reasonably believes the borrower has the ability to repay it…after carefully considering the facts along with the supporting documentation available to me, I am of the opinion that the bank has acted with due care and attention to this matter and consequently, I am unable to withhold your claim.”

Luckily, the Spanish Government yesterday passed a law stopping dangerously immoral people like Bjorlow from evicting vulnerable people like Anne.

Jyske’s historic relationship with Spain has traditionally been bumpy, to say the least. In 1994, they closed their Spanish branch for reasons we do not know. In 1999, they re-opened the branch with a view to serve the diverse expat communities investing heavily in Spanish property only to order its closure again in 2007, so that they could operate from the safety of Gibraltar it appears (cross-border service), and on the 26th of April 2010 they were fined by the Bank of Spain with 1, 7 million Euros for failing to comply with Spanish anti-money laundering provisions.

A while before, in 2004, the Supreme Court ruled against them by upholding a Court of Appeal ruling that ordered Jyske to pay an ex-employee compensation (€70,000), whose loan had been wrongly foreclosed because, even though it was agreed that whilst he worked for bank he would enjoy special terms and conditions, failing to pay higher interest when he left was not agreed as a “foreclosureable” default. As it happened, he had opted for a job with another bank which, clearly, was not of the liking of the bank. According to the Court, Jyske was found “…lacking good faith when exercising its rights under the mortgage loan contract”.

And not that long ago either, the Malaga Court of Appeal ruled that Jyske was not the owner of a company, Valiant Holdings, whose shares were pledged in guarantee of a loan repayment on a Spanish property. In spite of this, they chose to flatten the gardens, cut out the windows and close them up with wooden planks.

Last year, the Olive Press stepped in to help a victim of rogue trading and as recently as the 4th of October 2012, the Advocate General issued an opinion to the European Court of Justice, as requested by the Supreme Court on occasion of the appeal filed by Jyske Bank Gibraltar to the imposition of the 1, 7 million fine, to the extent that Spain has the right to exercise its right to supervise any bank operating in Spain, in respect of anti-money laundering provisions and any other matters of public interest, regardless of whether they are, or not, operating via a branch.

And we would not like to finish this post without a reference to what is going to be the very latest scandal to soon hit the headlines: the Equity Release tax-evasion fraud perpetrated by Jyske Bank Gibraltar.

Her name is Maria Tremurici-Falter and she has written millions of Euros worth of tax-evading equity release.

But we believe she must have resorted to other means to lure unsuspecting property owners to the Equity Release trap because the infantile sales-pitch below, surely, would have put anyone off straight away.

http://www.cyg-consulting.com/

CYG -CONSULTING GRUPPE (Specialized in Equity release) as a result of knowledge

Many years in contact with clients and financial institutions has taught me that there could be some problems – because of age, income…

What makes CYG -CONSULTING GRUPPE different: We are no magicians, but we try to find solutions – and sometimes it works.

Equity release: problems with the bank? Call us

Lifetime mortgage: you get monthly income and can not lose the property

Our experts in properties with “below market value” help investors to find the right investment (developments, plots, villas, hotels, commerce)

Special for English / Irish people: We offer QROPS / EURBS

In any case: Contact us. We will do our best, to help you!

The Bank of Spain has confirmed that Nordea Bank S.A. and Nykredit Realkredit A/S are abusing the Spanish legal system by selling mortgages and other bank products from their Representation Offices (Oficina de Representación) in Spain.

Because whilst both entities are registered with the Bank of Spain to carry out most of the banking activities throughout the UE via cross-border transactions, they are illegally selling banking products using their representation offices, for which article 10 of the Decree 1245/1995 provides that:

“Offices of representation will not be able to carry out credit operations, accept clients funds or offer financial intermediation, nor any other type of banking services, limiting the scope of their work to informative or commercial activities in respect of banking, financial or economic matters.”

Jesper Hertz, the man fronting Nordea Representation Office in Marbella and whose picture features on this site, has probably lost count of how many fraudulent equity release mortgages he has personally sold, through his Marbella office, and signed, via Spanish Notary Publics throughout Spain, despite this being strictly forbidden to him.

The reason they would do this is that it was cheaper for obedient Jesper to run around hunting potential victims and signing them up at the Notary offices, than to have Claus Jorgensen or Anders Woideman fly out to Spain to do the dirty job. They have been operating in this manner since 13/03/2002.

Christel Mark Hansen, working from the Nykredit Realkredit A/S Representation Office in Marbella, should have not lost count of the number of British clients she has personally advised on in respect of fraudulent equity release product as she personally visited their homes, would have a glass or two of wine and then sell them, with voracious appetite, very large non-status mortgages despite this being strictly forbidden to her.

The reason for this is that sweet-looking Christel would have hardly come across as someone selling a life-destructing financial product, in contrast to the Sydbank-tax-evading-thirsty-Swiss-based co-conspirators. They have been operating in this manner since the 14/09/2004.

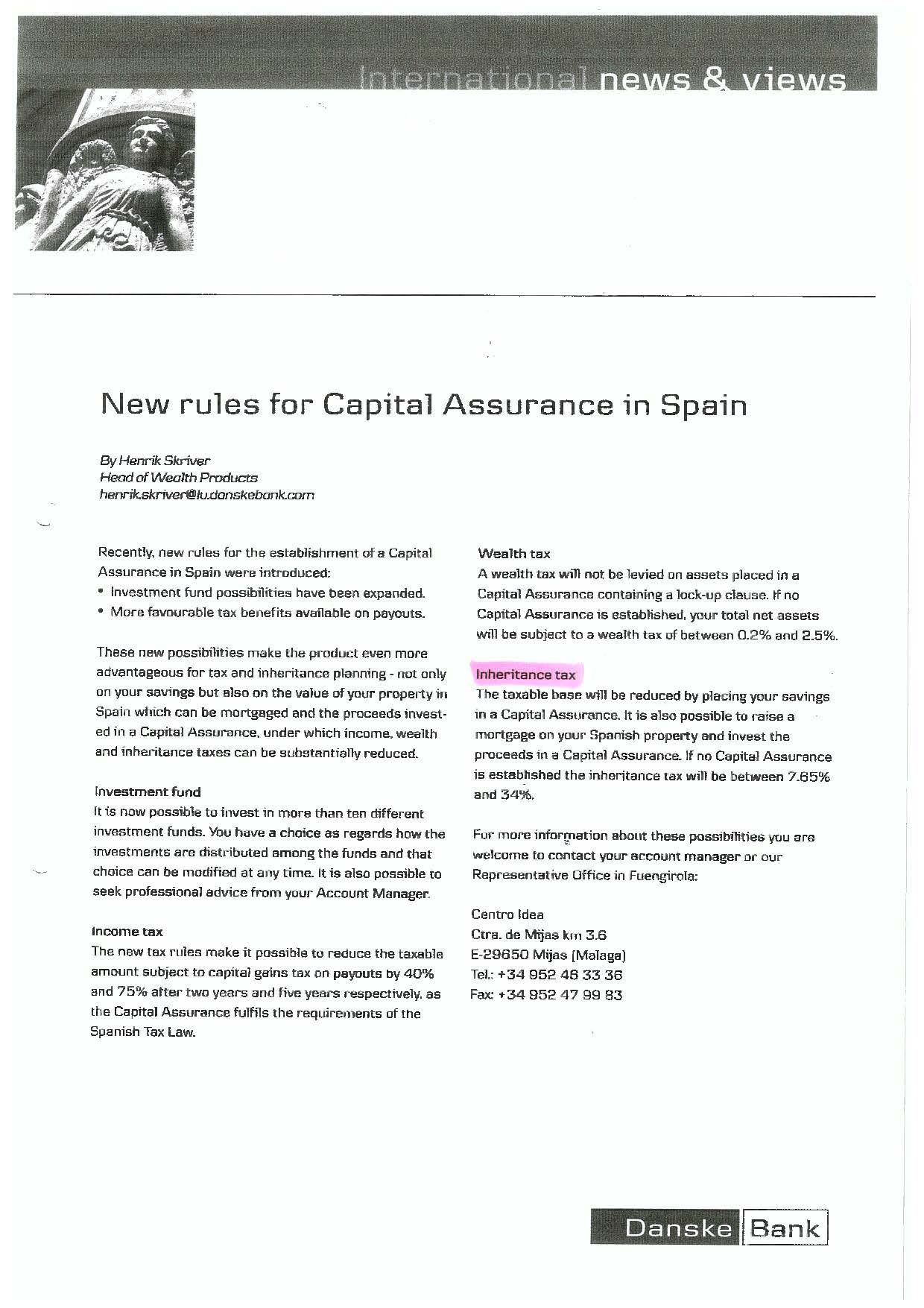

And Danske Bank International, also running their activities supposedly from Luxembourg, chose to set up a bogus “Representation Office” in Fuengirola to, as with competitors Nykredit and Nordea, sell and execute Equity Release Mortgage loans via the servile services of Henrick Hjerrild Hansen and John Lundskov Larsen. They have closed their office on the 15/01/2009.

So much for the Nordic Values…

Can you trust this man? Definitely not, if he is trying to sell you a mortgage + life insurance/capital assurance product.

Can you trust this man? Definitely not, if he is trying to sell you a mortgage + life insurance/capital assurance product.

Can you trust his company? As above.

Why? Because he will be lying through his teeth, as he has done in countless occasions in the past, and will tell you that this product is a fantastic opportunity for expats that have no mortgage on their properties as it will give them access to cash and also, eliminate taxes, none of which is true. Additionally, he will tell you that your property will never be at risk and that you should trust them because of their Nordic values, which he claims other bankers don’t enjoy. So far a few people have had their homes repossessed.

What do you mean by Nordic values? Nordea says that their company and staff are imbued of certain principles (integrity, impartiality, honesty, directness, flexibility and the ability to understand and treat clients like human beings), and that this differentiates them their competitors. If we interpret this literally, it would mean that bankers from say Afghanistan, Chile, Somalia or Spain lack integrity, are dishonest, biased and treat clients like animals…

What was this man’s role in the selling of Equity Release? Jesper Hertz was in charge of selling and signing off Equity Release products for Nordea Luxembourg in Spain. Wherever his company was not present, like in the Alicante/Murcia areas, he would reach out to potential customers through an agency network of rogue financial advisers, imposters who had easy access to the British expat community through years of presence on the Spanish Costas.

Did Jesper Hertz tell his customers that they would never lose their homes? Absolutely. Had he been transparent and honest, not one of his customers’ homes would have been at risk because not one would have signed the product, as simple as this. It was the obligation of Nordea, and Hertz, to specifically indicate their customers that this was a fraudulent product. On the contrary, Nordea’s mission was to come across as an elegant, sophisticated and trusted bank that would look after you to and, as they repeatedly insisted, preserve your wealth and look after your loved ones.

Their literature makes ludicrous and false statements such as : home sweet home…your most precious asset…keeping it in the family…our in-house specialists possess a deep and extensive knowledge of these virtues…we ensure that our advice is always open-minded, direct and honest so that we never promise you any more or any less that what is realistic…trust us…let us be your confidant.

You are talking about fraud, now that is a serious allegation! Jesper Hertz, from his office in Marbella, marketed, promoted and sold the virtues of a tax evasion cross-border service, similar in concept to the one UBS set in the US that cost them a criminal indictment (PDF). Although far modestly in means and resources compared to the Swiss bank, Nordea has still managed to create a refined set of promotional brochures that minutely explains how legal it is to register an artificial mortgage on your home, take the proceeds to a tax haven and have your inheritors receive the money abroad, without paying taxes, whenever you pop your clogs.

Why is it all wrong then? The problem is that you cannot register an artificial mortgage to make the tax authorities think that you have a real one, it is just illegal. And yet, Nordea Luxembourg organized a marketing campaign based on this premise. Secondly, it is wrong to tell your customers that you can inherit the proceeds of a life insurance/assurance product without paying taxes, quite simply because the law says that you pay IHT in Spain, whether you are a resident or a non-resident (and irrespective of the policy-holder being a resident or not).

How would you summarize Nordea Luxembourg Equity Release product? Tax cheating, customer deception and lack of values, all in one.

Jesper Hertz, Danish Chief Representative of Nordea’s one-man band Marbella office, did not allow 2 long-standing customers of the bank enter the office and equally, refused to provide them with the complaints book, which is obligatory.

Jesper Hertz, Danish Chief Representative of Nordea’s one-man band Marbella office, did not allow 2 long-standing customers of the bank enter the office and equally, refused to provide them with the complaints book, which is obligatory.

No sooner had he opened the door and saw the former Golf club friends than he was quick to give them the cold shoulder and ban them from accessing, what is -in short-, a public establishment. He then refused again to provide us with the complaints book on grounds that, being a Representation Office, they were not under such obligation and directed us to…Luxembourg. We obviously didn’t bother with the coffees.

Interestingly Nykredit Representation Office, just round the corner, did have the complaint book at the disposal of their cheated clients…

So the complainants had no option but to call the Local Police to report another token of Nordea’s legendary lack of compliance with Spanish laws.

It is now clear that all banks offered the Equity Release products as a way to reduce or eliminate Inheritance Taxes. They used, for that purpose, all manner of publicity, promotional literature, fliers, ads etc.

It now appears that this is not true, and yet banks say that even if they did make those assertions, the contracts said something different and as such, they would not be held liable. It transpires now that the law will allow Equity Release victims to demand that Inheritance Tax breaks do actually happen, pursuant to the old Consumers Association Act (valid till November 2007).

Shall they therefore be entitled to ask the Government to change the laws? Or rather, just ask the Judge to bin these scam contracts due to its fraudulent nature?

Article 8 stated the following:

Article 8

The offer, promotion or publicity of products, activities or services, will adjust to its nature, characteristics, conditions, utility or finality, without prejudice to what is established in the laws pertaining to publicity and in accordance to the principe of conformity with the contract regulated in its specific regulation.

Its content, the specific characteristics of each service or product and the conditions and guarantees offered, will be demandable by users and consumers, even where not expressly specified in the contract or in the document or receipt received.

Notwithstading the above, if the contract had more beneficial terms and conditions, these will prevail over the content of the offer, promotion or publicity.

The offer, promotion of false publicity of products, activities and services will be persecuted and fined as fraud. The Consumers Association will be authorized to initiate and intervene in the procedures legally established to ensure the banks cease to do so.

Strategic Asset Allocation was the pompous description coined by FINANSBANKEN A/S, taken over by Sparekassen Lolloland, to encapsulate a deceitful equity release product.

Strategic Asset Allocation was the pompous description coined by FINANSBANKEN A/S, taken over by Sparekassen Lolloland, to encapsulate a deceitful equity release product.

The sale of this financial sham was entrusted to a lady called Maria Tremurici-Falter, a Marbella socialite that does anything from complex financial products to charity expensive dinners or “knowing people”, and Michael (Mitch) Weisz, a mortgage broker who we cannot trace. They were both given a nice kick back of 1% of the value of the contract (at a minimum contract value of €1,000,000, not a bad day’s work!).

The below points give an idea of the monstrous set up Sparekassen Lolland came up with:

Article 27 of the Unfair Competition Act (Ley 3/1991 de Competencia Desleal) states that:

“…practices that convey inexact or false information in respect of the nature or size of the danger that a user or consumer or his/her family would be faced with, should he not take out the service or product, are equally deceitful, and will be deemed illicit”

Is this not what all these banks came up with?

Documents

Rothschild should have known a thing or two about mortgaging properties, one would have thought. And presumably one would have thought that, had Mr. Steven Dewsnip been in doubt as to the legality of his spurious Equity Release Scheme, sold as SPAIRS by a close collaborator (Henry Woods, illegal Costa financial operator), sound legal advice could have been easily accessed by the endless pot enjoyed by the Rothschild family.

Rothschild should have known a thing or two about mortgaging properties, one would have thought. And presumably one would have thought that, had Mr. Steven Dewsnip been in doubt as to the legality of his spurious Equity Release Scheme, sold as SPAIRS by a close collaborator (Henry Woods, illegal Costa financial operator), sound legal advice could have been easily accessed by the endless pot enjoyed by the Rothschild family.

And so they did, choosing the sixth Spanish firm by revenue, Gomez-Acebo & Pombo.

Interestingly though, the lawyer acting for the above firm (PDF), Mr. Luis Sánchez Pérez, failed to spot one very serious breach of Spanish Banking Laws incurred in by Rothschild: the document used to assess the value of the property (PDF) was not legal, since it was drawn up by a company not authorized by the Bank of Spain, under no circumstance, to produce valuations for mortgage purposes, in Spain.

His shortsightedness has only recently been exposed, after the ERVA closely inspected all documents delivered by victims of this sham, but far from trying to cover up he chose to indulge in publishing self-aggrandizement articles (PDF) that, coincidentally, talks about the…Spanish Equity Release.

This is what he says:

“world globalization allowed the reverse mortgage to be introduced in Spain, particularly with the first contigent of British expat that settled in the Spanish coasts…”

“the majority of the population that chose warmer climates have come to Spain to spend the best years of their lives, albeit with limited financial resources that are obvious in people who live off pensions and that, additionally, have seen the value of these dwindling as a result of the unfavourable exchange rates…”

“In situations where there is a lack of liquidity, a good option is the reverse mortgage…”.

In spite of dismissing the case shortly after it had been submitted, Fuengirola Court of First Instance has now agreed to implement a number of fact-finding requests on behalf of Euan Armstrong, as petitioned by his lawyers, after the initial dismissal was appealed successfully at the Malaga Appeal Court.

According to the decision of the Appeal Court, the dismissal of the criminal case against Danske Bank was found to be contrary to law because it was redacted in a laconic format incompatible with the Constitutional Tribunal doctrine and did not deal with the matters raised.

The Court of First Instance has now agreed to the following requests petitioned by EUAN ARMSTRONG’s Counsel: